LSD

Tech Heavy: Maybe Big Tech is not what we’re cracking it up to be?

The Nasdaq index was smashed last week, giving up 3.8% after Apple’s untimely demise at the hands of downgrading analysts. … Read More

The post Tech…

Investors just stripped on down and jumped headlong into Big Tech last year – the siren song of Artificial Intelligence and the saucy promise of falling cash rates proved too tempting.

But that was last year.

On Friday, most global indices ended in the red as rising US bond yields and a stronger-than-expected US jobs report murdered ’24 before it left the NYE dance floor.

In New York, stocks across the three US majors produced their first weekly loss since late October as US investors rushed to wind back their binge-bets on a recycling Fed.

But now we all have to deal with this.

This morning, there are just six stocks – Apple, Microsoft, Google daddy Alphabet, Bezos’ child Amazon, newcomer Nvidia, as well as Meta Platforms – with a united market cap of US$10tn, representing way over a quarter of the S&P 500’s total market valuation.

The US benchmark index gained 8% in 2023 – but its returns shrink to just 2% if you discount big tech.

That seems a little lopsided and is likely bad news for investors.

The tech heavy Nasdaq Composite index was absolutely bushwacked, giving up some 3.8% last week.

NASDAQ COMP ( weekly)

Next door, the S&P500 lost 1.8% and the Dow Jones lost 0.7%.

There are issues at play here beyond just overdoing it at Christmas time and the new, new bent on monetary policy.

Looming large are genuine fears for Q4 corporate earnings in the US, which unusually, appears to be weighing more on big tech stocks this time.

On that front, NVDA and AMD were among the only big names to emerge from this volatility, both up 1.8%, while APPL was squashed after attracting 2x analyst downgrades amid worries some of the shine has been lost.

In 2023, the iPhone maker racked up four straight quarters in a row of revenue shortfalls, which ate a hole in analyst confidence. Sluggish smartphone and PC sales seem proof of life.

On the upside, kind of, is that US Airlines rebounded for a second day after a seven-session losing streak, following that terrible, fiery Japan Airlines debacle in Tokyo.

American Airlines, Delta and United all soared over 3%.

The US Economic Calendar

The first full Wall Street trading week of 2024 also plays host to Day 1 of yet another US Q4 earnings season, which will officially kick off on January 12.

As per forever, it’ll be a story around US banks with Citigroup (C), JPMorgan Chase (JPM), Bank of America (BAC), Wells Fargo (WFC), and Bank of New York Mellon (BK) all featuring heavily.

This week the hair trigger gets pulled on US CPI numbers for December, due out on Thursday. The monthly US inflation read comes as traders re-lose their bottle around the likelihood and timing of the Fed’s idea of monetary policy.

The December CPI report is expected to show headline inflation and the core rate rising 0.3% month-over-month.

Other macro flashpoints in the States this week – data drops on consumer credit, the US trade balance, and the producer price index.

Monday January 8 – Friday January 12

MONDAY

Eurozone Economic Sentiment (Dec)

Eurozone Retail Sales (Nov)

United States Consumer Inflation Expectations (Dec)

Global Metal Users and Electronics PMI* (Dec)

TUESDAY

Japan Household Spending (Nov)

Japan Tokyo CPI (Dec)

France Balance of Trade (Nov)

Taiwan Trade (Dec)

Mexico Inflation (Dec)

Canada Trade (Nov)

United States Trade (Nov)

S&P Global Investment Manager Index (Jan)

WEDNESDAY

South Korea Unemployment (Dec)

China (Mainland) M2, New Yuan Loans, Loan Growth (Dec)

Philippines Trade (Nov)

Turkey Industrial Production (Nov)

France Industrial Production (Nov)

THURSDAY

South Korea BoK Interest Rate Decision

United States CPI (Dec)

United States Initial Jobless Claims

United States Monthly Budget Statement (Dec)

FRIDAY

Japan Current Account (Nov)

China (Mainland) CPI, PPI (Dec)

United Kingdom monthly GDP, incl. Manufacturing, Services

and Construction Output (Nov)

France Inflation (Dec, final)

India Industrial Production (Nov)

United States PPI (Dec)

Elon Watch

Elon enjoys life on the edge. But now, according to a Wall Street Journal report over the weekend, the execs and board members in Musk’s various creations are worried he’s going to trip off, literally.

My son lil X loves clinging precariously to my back & yelling “monkey rides!” pic.twitter.com/hzGXkBJk4X

— Elon Musk (@elonmusk) January 6, 2024

While Musk’s cannabis use is hardly a secret – he did after all smoke a reefer-joint (is what I believe the kids are calling it) on the top rating podcast of Joe Rogan – it’s the man’s more experimental private drug use of recent years, which the WSJ says is freaking not just Elon out.

Top execs have worried aloud that Musk’s use of mind bending illegal drugs could thwart the smooth and steady running of his six businesses, like the EV-maker Tesla, SpaceX, the former Twitter and an earth-drilling set up called The Boring Co. Drugs were certainly involved in the naming of that last one.

Citing sources close to Musk, the WSJ now says the billionaire routinely uses hard drugs like LSD, cocaine, ecstasy and psychedelic mushrooms at private parties.

Not wanting to draw attention to himself, all attending guests at any such event must first sign nondisclosure agreements and agree to give up their phones, the paper says in what’s supposed to be a massive scoop.

Of course, the rest of us know that we’ve been living in the 52-year old billionaire’s own private looniverse for years now. The scary part is really how much of the time he’s not tripping.

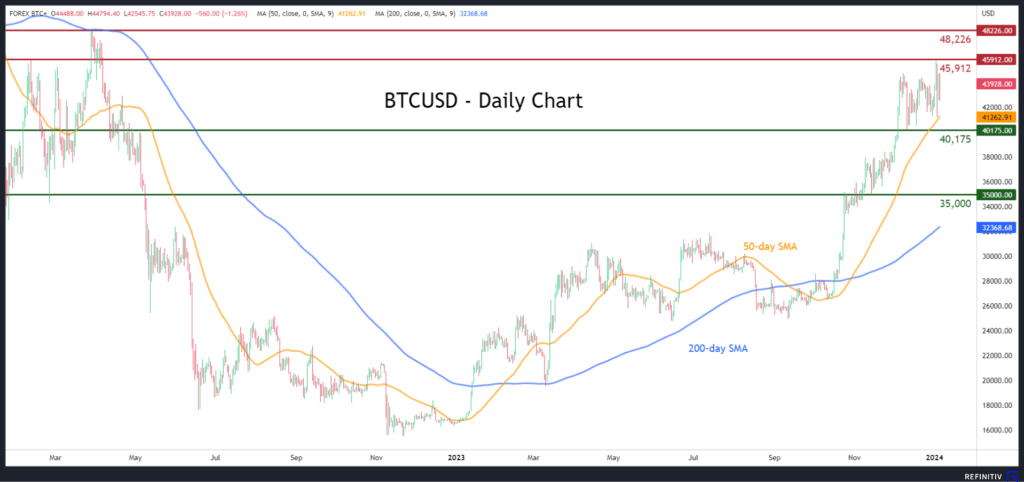

Bitcoin: New year, old habits

After a spectacular 2023, Bitcoin is behaving badly again as increasing anticipation of a green-lit spot Bitcoin ETF turns pineapple-shaped.

Tuesday last week, the cryptocurrency for adults leapt to US$45,912, its highest since April 2022. On Wednesday BTC then bequeathed its largest intraday loss since November 2022, after rumours that US regulators led by the Securities and Exchange Commission (SEC) were binning the ETF applications.

Peter McGuire of XM.com says although the sharp decline wiped out many leveraged positions, the bulls are now in for a push higher, regardless of any negative outcome in SEC’s upcoming decision.

“This quick recovery pretty much summarises the current state of the crypto market, with a ton of optimism already baked in despite the absence of actual proof that spot-Bitcoin ETFs will attract the anticipated institutional inflows in the industry.”

Undoubtedly, the buzz around the approval of spot-Bitcoin ETFs has been the main catalyst behind the latest bullish leg in crypto prices, but there are also other significant events in the 2024 calendar, Peter says.

“Hence, the market’s reaction both before and after the impending decision could serve as an example of what to expect moving forward.

“Specifically, there is speculation that the ETF approval might be a ‘sell the news’ type of event as crypto markets have rallied hard since BlackRock filed its first application back in summer, with the final decision acting as the perfect opportunity for some profit taking. Given that the Bitcoin halving event and Ethereum’s Dencun upgrade are scheduled to occur later in the year, crypto traders will remain on the edge of their seats as heightened volatility often creates opportunities for amplified gains.

“Although the year started with the best possible omens as Bitcoin posted a fresh 21-month peak of $45,912, the risks of a pullback are increasing due to the advance being significantly overstretched.”

“Should the medium-term rally resume, the price may revisit its recent 21-month high of $45,912. Failing to halt there, Bitcoin could face the March 2022 peak of $48,226.

“On the flipside, bearish actions could send the price lower to test the recent support of $40,175. Further declines might then cease at the November support of $35,000.”

US CPI: The Dot Sub-plot

The US dollar staged a decent recovery during the first week of the year, with market participants scaling back some basis points worth of rate reductions expected by December, although the total number of rate cuts anticipated by investors is still way larger than the amount of rate cuts indicated by the Fed’s December dot plot.

“At that gathering, the median dot for 2024 was revised down to 4.6% from 5.1% and Fed Chair Jerome Powell appeared more dovish than anticipated at the press conference following the decision. He said that rate increases are not the base case anymore and that the question now is ‘when will it become appropriate to begin dialling back?’

“With that in mind, at some point last week, investors were nearly fully convinced that a 25bps cut will be delivered in March and that interest rates should be lowered by 160bps by December. Now that number stands at around 140 and the probability of a March cut is down to around 70%.”

“Inflation has come down quickly in recent months due to weaker goods prices and moderating costs of services, including travel, even as rent increases remained elevated. Headline inflation saw a faster slowdown than underlying price pressures as energy prices began drifting south in September, erasing nearly all the gains posted during the summer months.”

There’s a ‘but’, Peter says. With the 2022 downtrend now dropping out of the year-on-year calculation, oil prices are close to their opening levels for 2023.

“Which means that the yoy change has moved from well into negative territory close to zero. And with the headline CPI rate resting well below the core one, even if the latter softens a bit more, this means that there are risks for a rebound in headline inflation.”

“Should this be the case, investors may further reconsider whether March is the appropriate time for a first rate reduction by the Fed, lowering the probability for that happening even further and scaling back more basis points worth of cuts for the whole year.

“Consequently, the US dollar could extend its recovery as Treasury yields edge higher,” according to the XM.com Australia CEO.

“Heading into this week, investors will be weighing several questions, including whether those rate cut expectations need to be dialled back. What does that mean to the first quarter S&P 500 estimates and multiple expansion discussions? For the broader market as a whole, it is nonetheless encouraging to see the sustained jobs growth, which is typically a lagging indicator of where the economy truly is.

“That question will be clearer following the fourth quarter results of the holiday shopping season,” Saintvilus says.

US Q4 Earnings Spotlight

Monday, January 8 – Jefferies Financial Group (JEF) and Helen of Troy (HELE)

Tuesday, January 9 – Albertsons Companies (ACI) and Acuity Brands (AYI).

Tilray Brands (TLRY) (Reports after the close)

Wall Street expects Tilray to report a per-share loss of 0.06 US cents on revenue of US$195.1 million. This compares to Q422 when the loss came to 11 cents EPS. Options trading suggests a double-digit swing in share price for pot stock.

Cannabis investors who backed Tilray have defo enjoyed the stock’s recent highs. TLRY – a Canadian cannabis company – surged close to 40% over the past six months, up 22% in the last month, but like all pot stocks, its long-term success depends almost entirely on favourable federal legislation.

Unfortunately, Canadian pot prices are slumping.

Wednesday, January 10 – KB Home (KBH).

Thursday, January 11 – Infosys (INFY).

Thursday, January 12 – UnitedHealth Group (UNH), JPMorgan Chase (JPM), Bank of America (BAC), BlackRock (BLK), and Bank of New York Mellon (BK).

Friday, January 13 – Delta Air Lines (DAL), Wells Fargo (WFC), Citigroup (C)

Wells Fargo (WFC) (Reports before open)

Wells Fargo stock jumped some 12% last month, beating with a bat the comparatively meagre 2.8% gain for the broader S&P 500. However while demand for commercial and industrial loans weakened in the first two months of the quarter, Wall Street expects Wells Fargo to double Q4 EPS (yoy) of US$20.34 billion in revenue at US$1.22 a pop. Q422 saw WFC deliver 0.61 US cents per share on revenue of US$19.66 billion.

The post Tech Heavy: Maybe Big Tech is not what we’re cracking it up to be? appeared first on Stockhead.

lsd

-

Psilocybin1 week ago

Psilocybin1 week agoAre Shrooms Legal in Oregon: Full Guide

-

Psychedelics1 week ago

Psychedelics1 week agoAtai Life Sciences Announces the Publication of Beckley Psytech’s Phase 1 Study of BPL-003 in the Journal of Psychopharmacology

-

Law & Regulation1 week ago

Law & Regulation1 week agoClearmind signs agreement with Hebrew University for psychedelic compound rights

-

Psychedelics1 week ago

Psychedelics1 week agoCybin Announces Publication of Research Manuscript in the Journal of Medicinal Chemistry

-

Psilocybin1 week ago

Psilocybin1 week agoCalifornia advances bill for psychedelics centers

-

Psychedelics1 week ago

Psychedelics1 week agoPsychedelics Can Offer More Than Therapy On Its Own

-

Psychedelics1 week ago

Psychedelics1 week agoRevive Therapeutics Announces FDA Acceptance of Meeting Request for Long COVID Diagnostic Product

-

Psilocybin4 days ago

Psilocybin4 days agoPassover Perspectives: Psychedelics, Moses, and the Burning Bush